04.14.26 By Bridgenext Think Tank

Insurers have invested millions in advanced pricing models and predictive analytics, yet underwriting results still lag. With combined ratios repeatedly crossing the 100 mark in recent years, and fewer than 20% of carriers fully trusting the data behind their underwriting decisions, the issue is no longer theoretical. It shows mispriced policies, inconsistent risk selection, and volatile loss ratios. The problem is not your modeling capability. It is the fragmented, inconsistent data feeding those models. Every disconnected risk record chips away at profitability, and every gap in risk identity weakens pricing precision, model trust, and growth. This is not just an IT or data quality issue. It is a profitability problem hiding in plain sight, and underwriters that unify their data are better positioned to capture the most profitable opportunities while others continue to absorb the cost of uncertainty.

The time to address this is now. Allowing fragmented data to shape underwriting decisions drains resources and grants market share to more agile competitors. The opportunity lies in exposing these hidden data leaks and turning your underlying architecture into a strategic growth advantage.

Read on to discover exactly how to identify these costly blind spots and build a resilient data foundation that protects your margins.

Imagine a single mid-sized commercial account that has three separate entities across your systems: one ID in policy administration, another in claims, and a third in billing. Your pricing engine reads the first record and assesses it as low exposure. However, the claims system, linked to a different ID, reveals a history of major losses. The underwriter spots the conflict and immediately overrides the model’s quote. This is master data management failure at its most destructive. This fractured identity occurs where the most critical business decisions happen. This is not just abstract, dirty data; it is misaligned identity directly eroding your margins and wasting the time of your most valuable talent.

The operational drag is severe and immediate. Today, 85% of underwriters still rely on manual spreadsheets during the pricing process, while 46% cite data cleansing as a primary barrier to success.1 When highly skilled actuaries and underwriters rank manual data entry as a top pain point, you have an efficiency crisis that actively stifles your growth and speed to market.

The business impact is undeniable: underwriting assumptions rest on mismatched inputs, and trust in your costly analytics investments quietly vanishes.

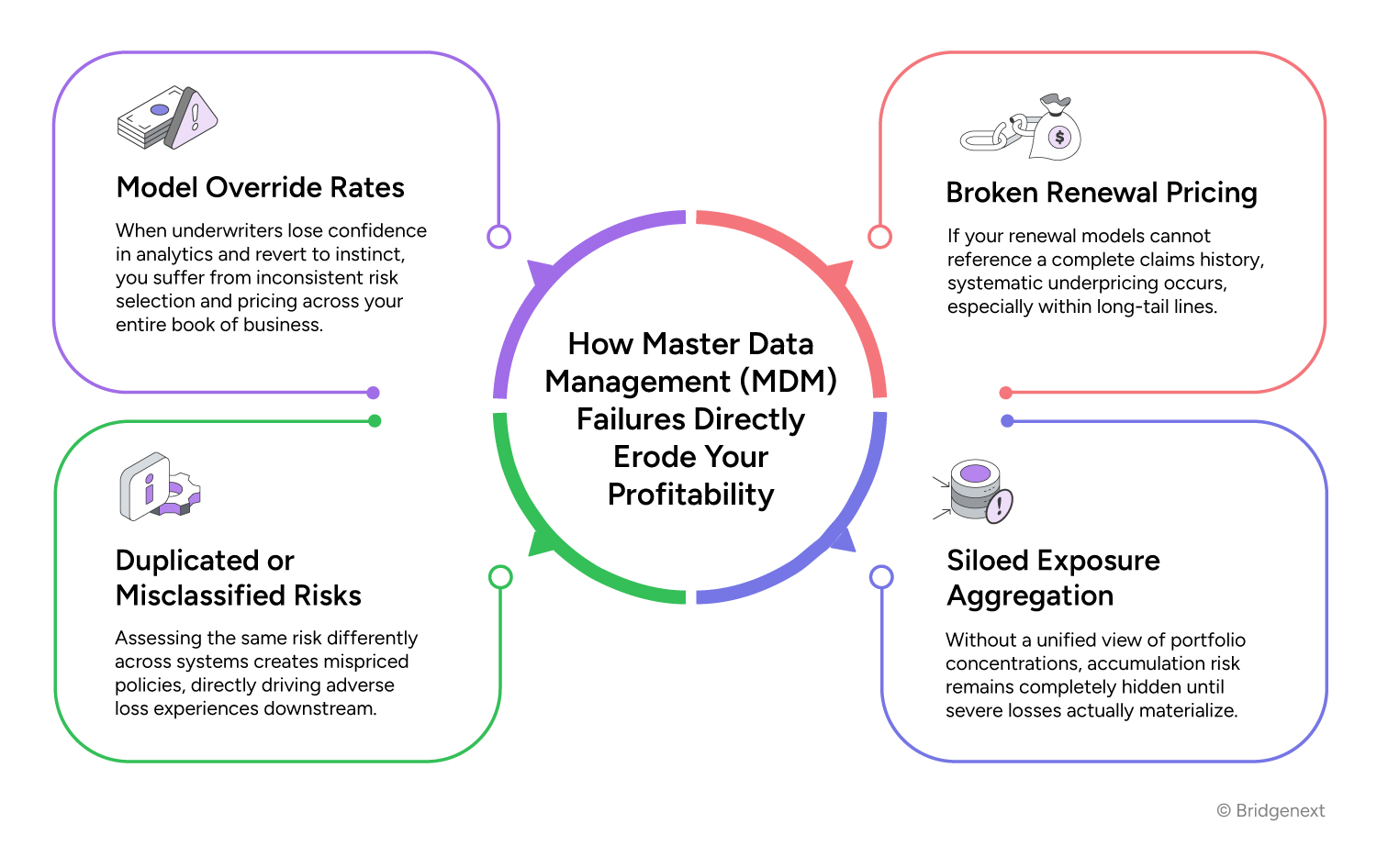

When data architecture breaks down, the financial impact ripples through every underwriting decision. Here is how Master Data Management (MDM) failures directly erode your profitability:

Individually, these might look like standard operational hurdles. Collectively, they cause a systemic erosion of underwriting discipline and act as a heavy drag on your bottom line.

Industry research highlights the massive stakes at play. Carriers that successfully integrate their data target 3–8 point improvements in loss ratio2, and leaders report 10–25% gains in operating profit from analytics.3 Yet those outcomes remain elusive for most insurers, not because the models aren’t sophisticated enough, but because the underlying data is still fragmented.

What looks like a back-office plumbing problem is a critical profit leak. Your competitors are optimizing their pricing models using unified, reliable data. By not focusing on your data architecture, you are handing more and more market share and margin to more agile competitors.

MDM fails because it’s typically framed and owned by the teams furthest from the pain. When MDM is treated as an IT or governance checkbox, it gets “data quality scores” but not executive support. Why? Because projects are scoped without tying them to underwriting outcomes. They’re measured in fields cleaned, not premiums saved.

Meanwhile, frustrated underwriters are ready to blame the model: one recent survey found 45% of underwriters say pricing models are “inaccurate or out of date”. The reality is that the model is only as good as its inputs. If MDM is judged by IT metrics instead of underwriting performance, it will never get prioritized. We need to flip the script: start with underwriting workflows and loss drivers, identify exactly where decisions break down, and trace those failures back to the missing data links.

This shift has a profound effect on scope and funding. MDM stops looking like just a data project and starts looking like a focused program to improve loss ratios and pricing consistency and thereby unlock growth. In short, MDM must be reframed from infrastructure to underwriting decision infrastructure. It then becomes an initiative owned by the business as well as IT, with KPIs like override rate and pricing dispersion, not just the number of records matched.

MDM, reframed as underwriting decision infrastructure, is not seen simply as a centralized data warehouse project. The project begins by anchoring on how underwriters really work. From there: unifying the risk entity so it flows across pricing, claims, billing, and exposure systems. Applying identity resolutions so actuarial models see clean, linked inputs, exactly as intended. Adding data lineage so underwriters and actuaries can trace a quote’s numbers back to the source, restoring their confidence.

The difference for the underwriter is striking. Before, they logged into multiple applications and mentally patched together conflicting information. After implementation, they see a single trusted risk view, complete with linked history and exposures. They no longer spend hours reconciling data; they are now positioned to ask better questions about the risk.

Success is then measured in business terms: fewer model overrides, tighter pricing consistency, lower loss-ratio variance, not vanity metrics of record cleanliness. Industry thought leaders agree. Deloitte’s 2026 Outlook explicitly warns that insurers must “prioritize data quality, integration, and master data management” to truly industrialize AI and analytics. In short, data integration isn’t a box to tick before transformation; it is the transformation.

The carriers closing the loss-ratio gap aren’t doing it with better models – they’re doing it with decision grade data infrastructure. If your underwriters are regularly overriding model recommendations, ask yourself: Is the model really at fault, or is the data behind it untrustworthy? MDM is the answer, but only if it’s reframed as a core business initiative that’s creating underwriting decision infrastructure, instead of just an IT hygiene project.

Insurers who connect their systems into a coherent, decision-ready data layer don’t just get cleaner data; they get smarter underwriting, more precise pricing, and margins that reflect actual risk. If model overrides, pricing inconsistency, or unexplained loss-ratio variance are showing up in your book, it’s time to fix the foundation.

Whether you’re struggling with fragmented risk identity, disconnected policy and claims systems, or analytics your underwriters don’t trust, Bridgenext can help you build the data foundation that makes every downstream investment pay off. Let’s start the conversation.

References:

1 www.carriermanagement.com/features/2025/12/23/282579.htm

2 www.swissre.com/press-release/New-digital-risks-call-for-insurance-innovation/be681945-d476-4b9d-a1ac-7222b978566e

3 www.mckinsey.com/industries/financial-services/our-insights/on-the-brink-realizing-the-value-of-analytics-in-insurance